Low temperature printed glass refers to glass substrates that are decorated, functionalized, or circuit-patterned using printing processes and inks designed to cure or sinter at relatively low temperatures compared with conventional ceramic frit and high-temperature enameling routes. These technologies enable printed graphics, coatings, conductive traces, resistive heaters, dielectric layers, and sensor patterns on glass without subjecting the substrate to high thermal loads that can cause warping, residual stress, or incompatibility with laminated, tempered, coated, or multi-layer glass stacks. Low temperature printing is increasingly important as glass becomes a multifunctional platform used not only for protection and aesthetics but also for electronics integration in automotive, architecture, appliances, and consumer devices. Between 2025 and 2034, the low temperature printed glass market is expected to expand steadily, supported by growth in automotive glazing and displays, smart building adoption, printed heaters and defogging systems, increasing use of decorative and branded glass in interiors, and rising demand for integrated sensors and functional coatings in next-generation glass assemblies.

Market Overview and Industry Structure

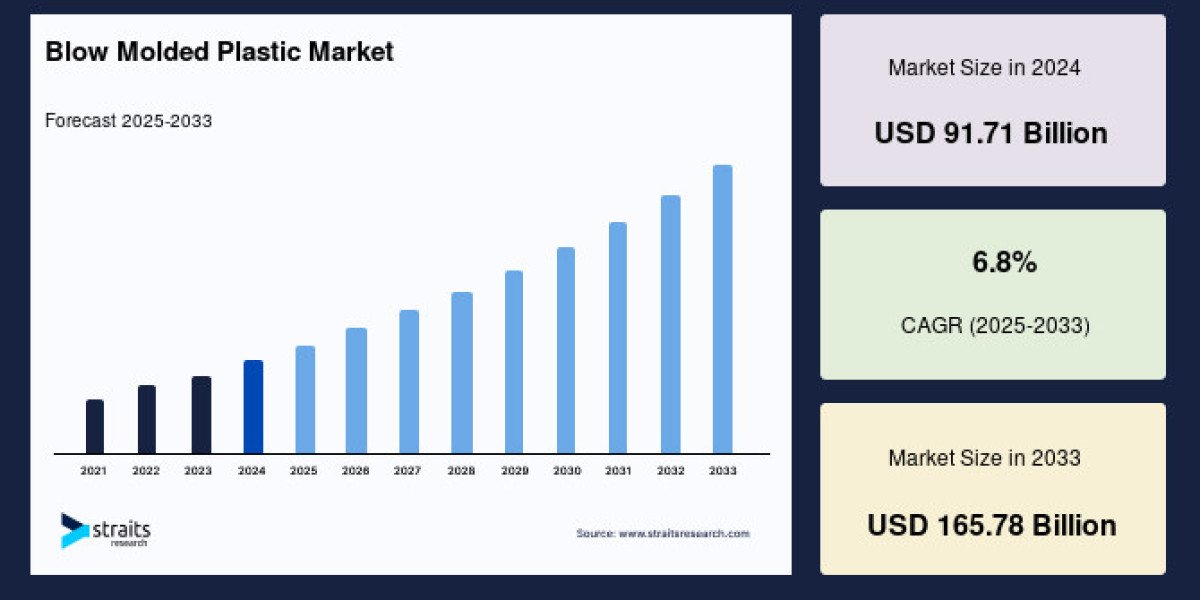

The Low Temperature Printed Glass Market was valued at $6.1 billion in 2025 and is projected to reach $10.4 billion by 2034, growing at a CAGR of 6.93%.

Low temperature printed glass combines glass processing with specialized printing technologies such as screen printing, digital inkjet printing, pad printing, and emerging functional printing methods that deposit inks or pastes onto glass surfaces. The inks may include UV-curable formulations, low-temperature curable organic-inorganic hybrids, nanoparticle-based conductive inks, and functional coatings tailored for adhesion, durability, and optical performance. Key performance factors include adhesion to glass, abrasion and chemical resistance, optical clarity or controlled opacity, conductivity or resistivity targets (for functional layers), and compatibility with downstream processing such as lamination, bending, tempering, or assembly into insulated glass units.

The industry structure includes glass processors and fabricators, specialty ink and paste suppliers, printing equipment manufacturers, and integrators that combine printing with lamination, coating, and cutting operations. In automotive, printed glass is often supplied through tiered supply chains where glass processors collaborate closely with OEMs and tier-1 suppliers to meet safety, durability, and optical requirements. In architectural markets, printing is integrated with façade and interior glass processing, often customized by project. In appliances and consumer products, printed glass is used for panels, doors, and control interfaces, requiring consistent cosmetics and long-term durability under heat, cleaning agents, and frequent handling.

Industry Size, Share, and Adoption Economics

Adoption economics for low temperature printed glass are driven by manufacturing flexibility, improved yield, and the ability to integrate functionality without expensive high-temperature processing. Low-temperature curing can reduce energy use and enable printing on glass stacks that include polymer interlayers, coatings, and laminates that would be damaged by high-temperature firing. This broadens addressable applications, especially where glass is already part of a layered assembly with sensitive components.

In decorative applications, the value is linked to customization, branding, and aesthetics, enabling high-resolution graphics and shorter production runs through digital printing. In functional applications such as printed heaters, defoggers, and conductive patterns, value is driven by performance integration and reduced part count, enabling simplified assembly and improved reliability. Market share tends to concentrate among suppliers that can consistently deliver adhesion, durability, and optical quality at scale, and among ink suppliers that provide stable formulations compatible with high-volume production and demanding qualification standards.

Key Growth Trends Shaping 2025–2034

A major trend is the electrification and digitalization of vehicle interiors and exteriors. Automotive glass is increasingly integrated with sensors, antennas, defogging heaters, and display-related features, and low-temperature printing supports functional patterns that can be integrated into laminated or coated glazing systems. Growth in panoramic roofs, larger windshields, and advanced driver assistance systems supports demand for printed patterns that manage glare, integrate conductive features, or support sensor placement.

Smart buildings and architectural design trends are also driving growth. Printed glass is used for decorative façades, privacy patterns, branded interiors, and functional coatings for glare management and thermal comfort. Low temperature printing supports customization and shorter lead times, particularly for project-based construction. In addition, demand for smart glass features such as transparent heaters, defogging, and integrated lighting or signage can expand functional printing adoption.

Appliances and consumer interfaces represent another growth channel. Glass is increasingly used in premium appliance doors, cooktop panels, and control surfaces. Low temperature printed functional layers can enable capacitive touch interfaces, illuminated icons, and printed heaters or anti-fog features while maintaining design aesthetics. Digital printing also supports mass customization and faster design refresh cycles in consumer products.

Technology innovation in inks and curing methods is a further trend. Nanoparticle conductive inks, low-temperature sintering approaches, and UV-curable hybrid chemistries are improving performance and durability. Equipment advances such as high-precision inkjet deposition, inline curing, and automated inspection are improving throughput and defect detection, which is critical as functional printed layers require tighter control than purely decorative printing.

Core Drivers of Demand

The primary driver is the shift toward multifunctional glass in automotive, buildings, and appliances. As glass becomes an interface and functional component, printing enables integration of visual and electrical features directly on the substrate. A second driver is manufacturing efficiency and energy savings: lower curing temperatures reduce energy consumption and expand compatibility with laminated and coated glass stacks. A third driver is customization and design differentiation, particularly in architecture and premium consumer products, where printed glass supports distinctive aesthetics and branding.

Reliability and integration also drive demand. Printed functional layers can reduce the number of separate components, connectors, and assembly steps, improving long-term durability. In automotive and appliances, this integration approach supports simplified supply chains and improved product robustness.

Browse more information

https://www.oganalysis.com/industry-reports/low-temperature-printed-glass-market

Challenges and Constraints

The market faces constraints around durability, qualification, and process consistency. Low temperature inks must deliver long-term adhesion and resistance to abrasion, moisture, UV exposure, cleaning chemicals, and thermal cycling. In automotive and outdoor architectural use, weathering performance and safety compliance requirements are strict. Achieving consistent curing and uniform properties across large glass areas can be challenging, especially for conductive and resistive patterns where variability affects performance.

Another constraint is the trade-off between low-temperature curing and ultimate film robustness. High-temperature fired ceramic frits have proven long-term durability in harsh conditions; low-temperature systems must match or exceed those benchmarks in targeted applications. Conductive ink performance can also be affected by oxidation, microcracking, and interface stability, requiring careful formulation and protective layers.

Cost and scalability can be constraints, particularly for advanced conductive inks that rely on precious metals or specialized nanoparticles. For high-volume markets, throughput and yield are critical; defects in printed functional layers can cause rejection of high-value glass panels. Finally, integration complexity can slow adoption. Printed functional glass must align with downstream lamination, bending, and assembly steps, and supply chain coordination is essential to maintain performance.

Market Segmentation Outlook

By printing technology, the market includes screen printed glass, digital inkjet printed glass, and hybrid printing approaches combining multiple deposition methods. By application, segments include decorative architectural glass, automotive glazing (defoggers, frit patterns, sensor-related patterns, antennas), appliance and consumer interface glass, printed heaters and resistive elements, and specialty industrial and laboratory glass with functional patterns. By end user, major segments include automotive OEMs and tier suppliers, architectural glass fabricators and façade contractors, appliance manufacturers, and electronics and industrial equipment producers. By ink type, segments include UV-curable inks, low-temperature cured organic-inorganic hybrids, nanoparticle conductive inks, and dielectric or functional coating formulations.

Key Market Players

- Dip-Tech Digital Printing Technologies

- AGC Inc.

- Saint-Gobain

- Guardian Glass

- NSG Group

- Asahi Glass Co., Ltd.

- Ferro Corporation

- Vasiliou Glass Technology

- Glassolutions

- Interpane Glas Industrie AG

- Sejal Glass Ltd

- Kerajet S.A.

- Torrecid Group

- Xinyi Glass Holdings Limited

- NorthGlass

Competitive Landscape and Strategy Themes, Regional Dynamics, and Forecast Perspective (2025–2034)

Competition is driven by print quality, functional performance consistency, durability, and process integration capability. Leading players differentiate through advanced printing lines, inline inspection and automation, strong process control, and the ability to qualify products for automotive and architectural standards. Ink suppliers differentiate through adhesion chemistry, durability performance, conductivity targets, and compatibility with high-speed printing and curing. Strategic themes through 2034 include developing more durable low-temperature ink systems, improving conductive ink cost-performance, expanding digital printing capability for mass customization, and integrating printing with lamination, coating, and sensor assembly workflows. Suppliers are also expected to invest in sustainability, reducing energy consumption and improving waste management in printing and curing operations.

Regionally, Asia-Pacific is expected to be a major growth engine due to automotive production, electronics manufacturing ecosystems, and large-scale architectural development, alongside strong glass processing capacity. North America is expected to see steady growth driven by automotive innovation, premium appliances, and architectural refurbishment and smart building projects. Europe is expected to grow steadily with strong demand for design-led architectural glass and advanced automotive glazing systems, supported by sustainability-driven building upgrades. Other regions will see selective growth tied to infrastructure development, automotive assembly expansion, and adoption of premium glass-based interiors.

From 2025 to 2034, the low temperature printed glass market is positioned for steady expansion as glass evolves into a multifunctional platform integrating aesthetics, interfaces, and electrical functionality. Growth will be strongest in automotive functional printing, smart building and decorative architectural applications, and appliance interface glass. Suppliers that deliver durable low-temperature ink systems, high-yield manufacturing, and strong integration with downstream glass processing will be best positioned to capture durable growth as customers increasingly demand high-performance, design-forward, and energy-efficient printed glass solutions over the forecast period.

Browse Related Reports

https://www.oganalysis.com/industry-reports/glass-reinforced-plastics-grp-pipes

https://www.oganalysis.com/industry-reports/engineered-foam-market

https://www.oganalysis.com/industry-reports/polypropylene-twine-market

https://www.oganalysis.com/industry-reports/encapsulation-resins-market

https://www.oganalysis.com/industry-reports/low-density-polyethylene-market